The input credit system under GST greatly reduces the total tax that a business would owe. However, taxpayers are often confused by having access to 2 different statements in the GST Portal (GSTR-2A and GSTR-2B). Understanding these statements is important, as they both affect ITC reconciliation and compliance with GST regulations.

If you have ever searched for the difference between GSTR 2A and 2B, you're not alone; many accountants, business owners, and GST practitioners don't understand how these two reports work when they want to correct their input tax credits reports. This document aims to clarify GSTR 2A and GSTR 2B so that your decisions about filing your GST return are informed by the best information available.

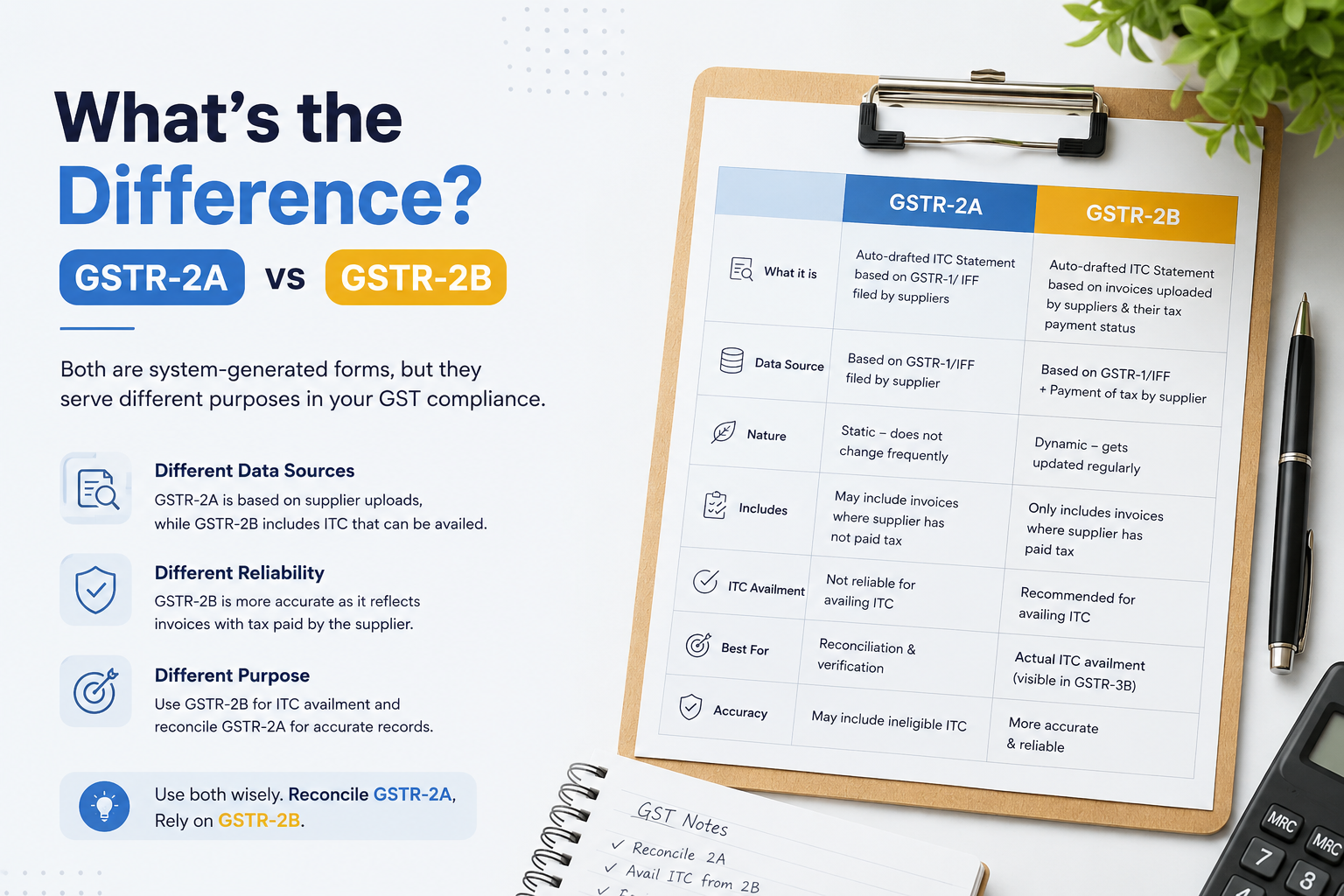

Understanding GSTR 2A

The GST portal provides access to an auto-created statement called GSTR 2A. GSTR 2A contains information on all the inward supply (goods received) by a taxpayer. This information is received from the suppliers of the taxpayer and is based upon GST returns submitted by suppliers.

GSTR 2A is dynamic: every time a supplier completes a new return, amends an invoice, or uploads a missing invoice/good in the system, the information in GSTR 2A will change. Therefore, GSTR 2A is continually updated.

For example, if your supplier failed to upload an invoice for March but did upload it the following month, you will see the invoice appear in GSTR 2A after May's return was submitted. Because of the dynamic nature of GSTR 2A, taxpayers will typically have difficulty using their GSTR 2A as a final reference point for claiming ITC on purchases.

The statement includes details such as:

- B2B invoices

- Credit notes

- Debit notes

- Import details

- Amendments made by suppliers

- Information submitted through various GST returns

Although GSTR 2A provides comprehensive transaction details, its continuously changing nature can create confusion during monthly reconciliations.

What Is GSTR 2B?

Many taxpayers ask, what is GSTR 2B and why it was introduced when GSTR 2A already existed.

The GST Department generates a static, auto-generated ITC statement called 'GSTR 2B' to simplify reconciliation for tax credits. GSTR 2B is similar to GSTR 2A; however, GSTR 2B will not change for the relevant tax period, and will remain fixed after being created

To understand GSTR 2B, think of it like this statement that kind a gives taxpayers a clear view of eligible, and not eligible, input tax credit for a given month. Once it is produced, this report doesn't get altered even if the suppliers do amendments later or file a modified paper. you know, it stays as it was.

This feature makes GSTR 2B highly reliable for GST return filing because businesses can easily determine the amount of ITC available for claim.

The statement categorizes tax credits into different sections, helping taxpayers identify:

- Eligible ITC

- Ineligible ITC

- Reversed ITC

- Import transactions

- ISD credits

- ITC from suppliers

Since the data remains constant for a specific tax period, businesses can perform reconciliations more efficiently.

Difference Between GSTR 2A and 2B

The difference between GSTR 2A and 2B primarily lies in the way data is generated and maintained.

GSTR 2A is sort of dynamic, and it keeps getting updated all the time whenever suppliers upload or change invoice info. While GSTR 2B is static, and it gets generated only one time for that tax period.

So, when you compare 2A vs 2B, the key thing is that GSTR 2A shows the near-real time supplier details, while GSTR 2B gives a settled snapshot of the Input Tax Credit that is available.

Additionally, the purposes of the two documents differ greatly. GSTR 2A serves as a reference in determining whether suppliers have complied with their obligations and tracking transactions. The GSTR 2B is primarily for identifying the exact amount of ITC that should be claimed by taxpayers in their returns.

For companies dealing with huge invoice counts, GSTR 2B usually makes reconciliation easier because once it’s out, the numbers do not shift or wobble, basically after generation.

Why GSTR 2B Is Preferred for ITC Reconciliation

Over the years, GST compliance has evolved to improve transparency and reduce mismatches in tax credits. As a result, GSTR 2B has become the preferred statement for ITC reconciliation.

When businesses rely solely on GSTR 2A, frequent data changes may lead to discrepancies during return filing. Since suppliers can update invoices at any time, the reported figures may vary from one day to another.

GSTR 2B addresses this issue by providing a fixed statement for a specific tax period. Taxpayers can reconcile purchase records with confidence and identify missing invoices before filing returns.

This is one reason why professionals frequently explain the gstr 2a and 2b difference to clients and recommend using GSTR 2B as the primary source for ITC calculation.

Practical Example

Suppose a business purchases goods from a supplier in April. The supplier forgets to upload the invoice while filing GST returns for April and instead reports it in May.

In GSTR 2A, the invoice will eventually appear once the supplier uploads it. Since GSTR 2A updates dynamically, the statement changes accordingly.

However, GSTR 2B for April will not include that invoice because it was not reported within the relevant period. The invoice may appear in the subsequent GSTR 2B statement based on GST rules and reporting timelines.

This example clearly demonstrates the difference between GSTR 2A and 2B and highlights why businesses should regularly review supplier compliance.

Benefits of Using GSTR 2B

GSTR 2B provides several advantages for taxpayers. It helps simplify return filing, improves accuracy, and reduces reconciliation efforts.

Since GSTR 2B means a fixed ITC statement for a particular tax period, businesses can easily match purchase records and identify discrepancies. The statement also minimizes the risk of claiming excess or incorrect tax credits.

Furthermore, the GST portal clearly classifies eligible and ineligible credits, helping taxpayers comply with GST regulations more effectively.

These benefits have made GSTR 2B an essential tool for accountants, tax consultants, and business owners across India.

Which Statement Should You Use?

Both GSTR 2A and GSTR 2B will be of value when reconciling any ITC and filing GST returns; however, many GST experts recommend GSTR 2B as the preferred method for reconciling ITC and filing GST returns due to its accuracy. GSTR 2A, however, can still assist in tracking supplier uploads and monitoring an invoice's status.

Businesses should ideally review both statements regularly. GSTR 2A helps identify whether suppliers have uploaded invoices, while GSTR 2B provides the final basis for claiming input tax credit.

Understanding the difference between 2A and 2B allows taxpayers to maintain accurate records and avoid GST compliance issues.

Conclusion

GST payer should be familiar with the differences between GSTR 2A & GSTR 2B. GSTR 2A contains dynamic information on all transactions from suppliers that have reported sales directly to GST (e.g., through their own return) whereas GSTR 2B gives you a more static picture to allow reconciliation & verification of ITC on purchases made during the relevant tax period.

GSTR 2B is basically an ITC statement that provides an easier way for taxpayers to comply with their GST obligations by filing their correct ITC claims. Knowing the difference between GSTR 2A and 2B will help businesses avoid making reconciliation errors, receiving notices or facing unnecessary compliance challenges as a result of their mistakes.

Since GST rules keep changing, it’s kinda useful to treat GSTR 2B like your main ITC cue and keep an eye on GSTR 2A, so you can check supplier compliance too . This combo should help make your GST return filing smoother, and more accurate.